Let’s understand what Monopoly and Perfect Competition is first and then we can point out what their differences are.

Monopoly: In a monopoly there is just one firm who has captured the entire market of a particular product or services and do not have any competitor as such. Hence, the producer has the capacity to set the price he wants for his profit maximization. Since there are many buyers for that product or service the producer will always face inelastic demand. To understand demand elasticity please see the post here.

Perfect Competition: In a competitive set up there are many producers and hence each one of them just capture a fragment of a market of a product or a service. So they cannot set or change market price. There are many buyers and the producers face a completely elastic demand curve which means if a seller or a producer charge a higher price than his competitors he will lose his market share because then the buyers will choose to buy from other sellers. As simple as that!

Now let’s look at the table above which shows the total revenue and total cost for producing the mentioned units of outputs.

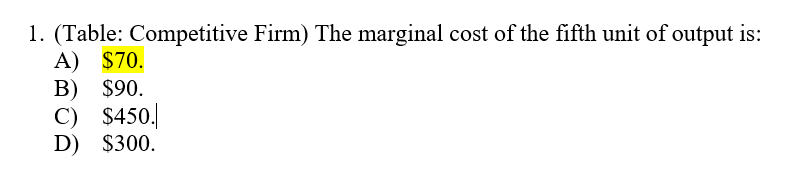

The first question asks the marginal cost of the 5th unit of output. The answer will be 300-230 =70. Concept used : Marginal Cost = cost of producing 1 extra unit of output.

Fixed cost is something which is incurred even before producing 1 single unit of output. So it will be 50.

The answer to this question is 450-360 =90. Concept used: Marginal Revenue = revenue earned from 1 extra unit of output sold.

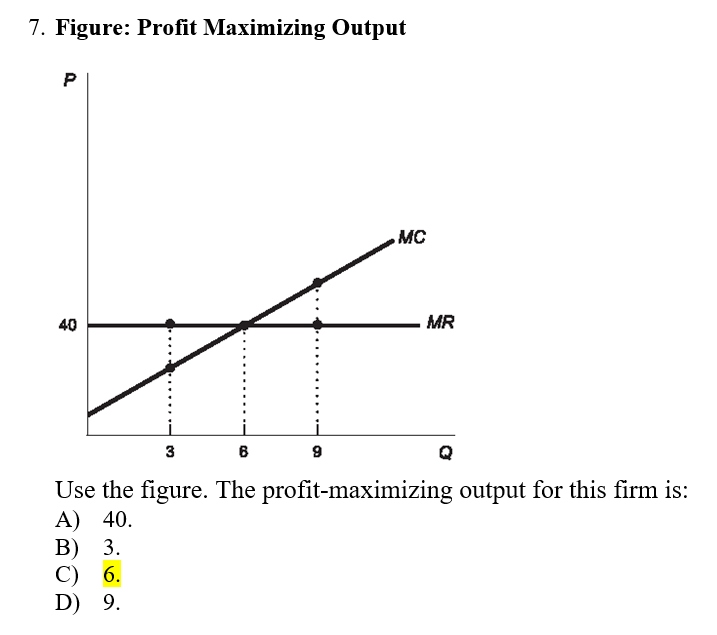

Let’s look at a simple question on profit maximization:

The profit maximization occurs where marginal revenue equals to marginal cost i.e. where one additional unit of producing an output equals to the cost of producing that extra unit. So profit maximizing price is 40 and quantity is 6.

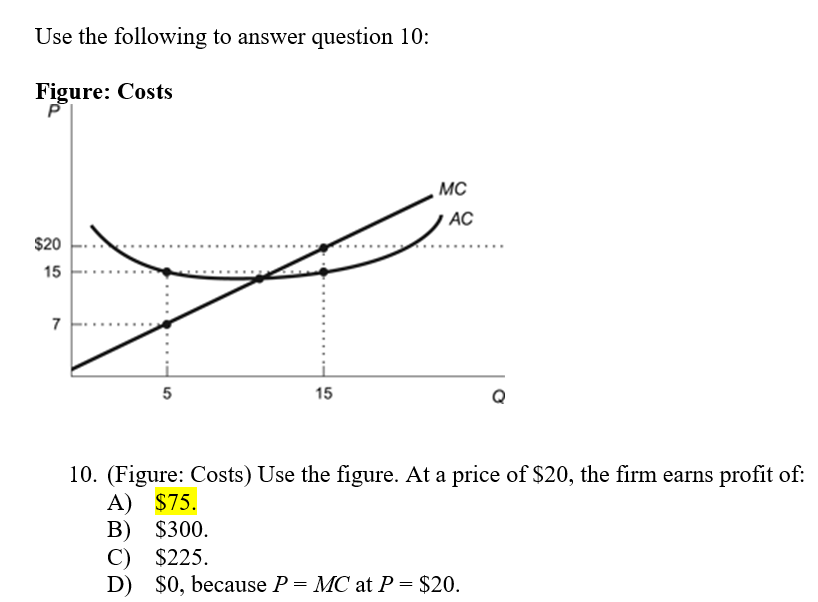

In the above question, at price 20, Revenue = 20*15 =300. Now to produce those 15 units of output, Total cost =Average cost * quantity produced =15*15 =225.Hence, Profit = total revenue -total cost = 300-225 =75.

Economic profits may be positive, zero, or negative. If economic profit is positive, other firms have an incentive to enter the market. If profit is zero, other firms have no incentive to enter or exit. When economic profit is zero, a firm is earning the same as it would if its resources were employed in the next best alternative. If the economic profit is negative, firms have the incentive to leave the market because their resources would be more profitable elsewhere. In the short run, a firm can make an economic profit. However, if there is economic profit, other firms will want to enter the market. If the market has no barriers to entry, new firms will enter, increase the supply of the commodity, and decrease the price. This decrease in price leads to a decrease in the firm’s revenue, so in the long-run, economic profit is zero. An economic profit of zero is also known as a normal profit. Despite earning an economic profit of zero, the firm may still be earning a positive accounting profit.

For Perfect competition there are many sellers and many buyers. Products are same and the sellers are price takers which means they cannot change the price much otherwise they will go out of business. Product differentiation occurs only in case of monopolistically competitive markets.

In a perfectly competitive industry sellers cannot manipulate the price. So to maximize profit they will have to charge what their competitions are charging.

I will post some more solved questions on Market structure in another post.