Market is a place where the forces of demand interact with the forces of supply to determine the market clearing price and quantity transactions. Consumers are utility maximisers, and producers/suppliers are profit maximizers. In equilibrium, two equal and opposite forces are in harmony.

Key factors determining Economic Demand:

- Own price of the commodity is the prime determinant of the demand for the product keeping other things constant. If the price of a commodity falls, the quantity demanded of it rises and vice versa according to law of demand. Mathematically the demand function is written as D = D(P), where D’ <0.

- Average income of consumers has a positive relationship with the demand for a normal commodity. As the average income rises in society, people demand more of that commodity. However, when the demand of a commodity falls despite of an increase in average income of the consumers that commodity is known as inferior commodity.

- Prices of other commodities and their availabilities matter too. The demand for a commodity rises when the price of a substitute product rises or when the price of a complementary product falls.

- The market size or number of consumers influence the demand for any commodity. For example – the demand for rice is higher in India compared to United States.

- Income distribution in the society impacts the consumption demand in market quite a lot. As the income distribution becomes more and more equitable consumption demand rises more and more because of the marginal propensity to consume is comparatively higher among poorer sections of the society.

- Behavioral patterns of consumers matter too. Some people may get influenced by others’ choices, some may take a higher price as a signal of higher quality etc. and all these factors together may impact the market demand.

- If people are speculating the price movement of a product, e.g. in share market there are intense speculations and those speculations highly influence the price movement.

- Government policies and regulations often dictate market demands. Governments often use tax as an instrument to raise (or lower) the market demand for macroeconomic stabilization. Often for products like alcohol or cigarettes the taxes are higher to curb down demand.

Derivation of Market Demand Curve :

Market demand curve is obtained from the individual demand curves by the horizontal summation rule. If at a price point 10 consumer 1 purchases 5 packets of chips and consumer 2 purchases 8 packets of chips, then the market basically purchases 12 packets of chips. Horizontal summation rule is based on the assumption that individual choices are independent and free from any bias.

Some typical cases of Supply Curves :

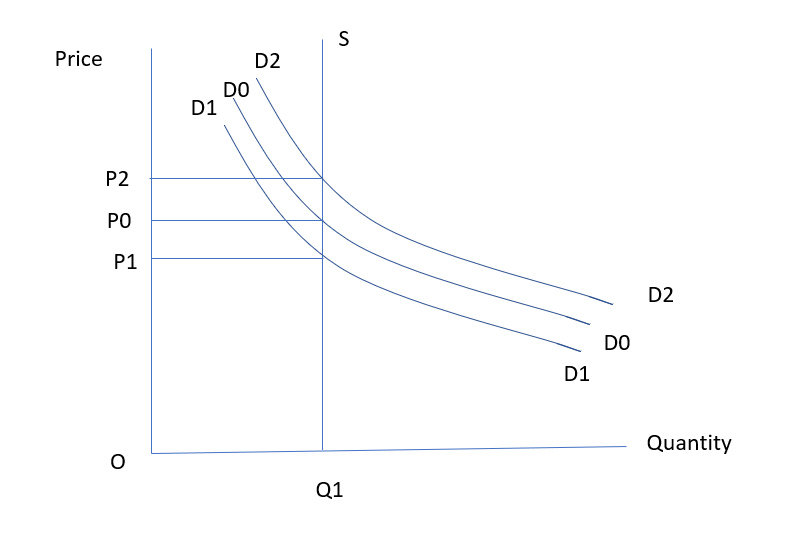

Case 1 : A full employment supply curve is vertical which is perfectly price inelastic.

If D0D0 is the initial demand curve equilibrium price and quantity will be OP0 and OQ1 respectively. Now if demand rises (or falls) to D2D2 (or D1D1) the equilibrium price rises (or falls) to OP2(or OP1) but the equilibrium output will remain unchanged at OQ1.

Case 2 : Perfectly price elastic supply curve

In a perfectly competitive labour market, employer finds the labour supply curve to be perfectly price (actually wage in this case) elastic. Being a small purchaser of labour he can have any amount of labour at the given wage rate OW.

Some typical cases of Demand Curve:

Case 1: Perfectly Price elastic demand curve

A perfectly competitive producer/seller finds the demand for his product/services to be perfectly price elastic. The producer being a small supplier of homogeneous product can sell whatever he wants in order to maximize his profit at the given market price OP1.

Case 2: Perfectly Price inelastic demand curve

If the demand curve is perfectly price inelastic as happens in the case of necessary goods like life saving medicines, everyday basic food products etc., supply changes impact only equilibrium price and not the quantity.

Conclusion

Markets are dynamic arenas where the motivations of consumers and producers intersect, and prices act as the balancing force. Demand and supply curves—shaped by factors like income, preferences, expectations, production constraints, and government policies—determine how resources are allocated and at what cost. Understanding the nuances of demand, from the law of demand to behavioral influences, and the nature of supply, whether perfectly elastic or inelastic, equips us with critical tools to analyze real-world market behavior. As economies evolve and markets face new shocks, these fundamental principles remain vital in explaining how equilibrium is established and how deviations can lead to larger economic implications. Mastery of these concepts is foundational for anyone exploring economics, policymaking, or market strategy.